Car factories idled for the best part of two months; car dealerships closed; over 36 million unemployed in the US, and many millions more furloughed or laid off worldwide—with so few people buying cars at the moment, there is no real urgency to build more, other than to get the industry as a whole moving again.

The picture looks bleak for the global automotive industry, and in particular for automotive suppliers, but the slow yet inevitable transition to electrification combined with the impact of the novel coronavirus (COVID-19) paints a particularly bleak picture for the supply of engines. In terms of output, automakers ended 2019 looking back longingly to the peaks of a few years earlier, with global vehicle production in 2019 already in decline before the coronavirus struck. This slackening of demand (‘Vehicle assembly was falling—and then came COVID-19‘) reflected a downward trend in global vehicle sales that began in 2018 with weakening in key markets, notably China. Engine output largely follows trends in vehicle output and demand, and in 2019, vehicle output was down by around 5% year-on-year to 88 million units.

According to new Automotive World research, engine production in 2019 fell by 4.4% year-on-year, with output of light and heavy vehicle engines totalling just shy of 83.2 million units, compared to 87 million a year earlier.

Whatever happened before COVID-19 is a mere bagatelle to the impact the pandemic will have on vehicle demand in and after 2020

In Europe, three of the region’s engine plants produced over 1.5 million units in 2019: PSA Tremery in France (1.75 million), VW Salzgitter in Germany (1.58m) and VW’s Györ, Hungary factory (1.97m). Other significant engine manufacturing operations, building 1 million units or more in 2019, were BMW’s Steyr, Austria plant (1.23m), two of Daimler’s German engine plants, namely Bad Cannstatt, Stuttgart (1.18m) and Koelleda (1.14 m), and Renault’s Valladolid plant in Spain (1.36m).

Outside Europe, Toyota operates two ‘millionaire’ engine plants in Japan, at Kamigo (1.25m) and Shimoyama (1.05m); Suzuki’s Sagara plant assembled one million engines in 2019. In North America, FCA’s Saltillo plant in Mexico made 1.09 million engines, and Honda’s Anna, Ohio facility in the US built 1.08 million engines.

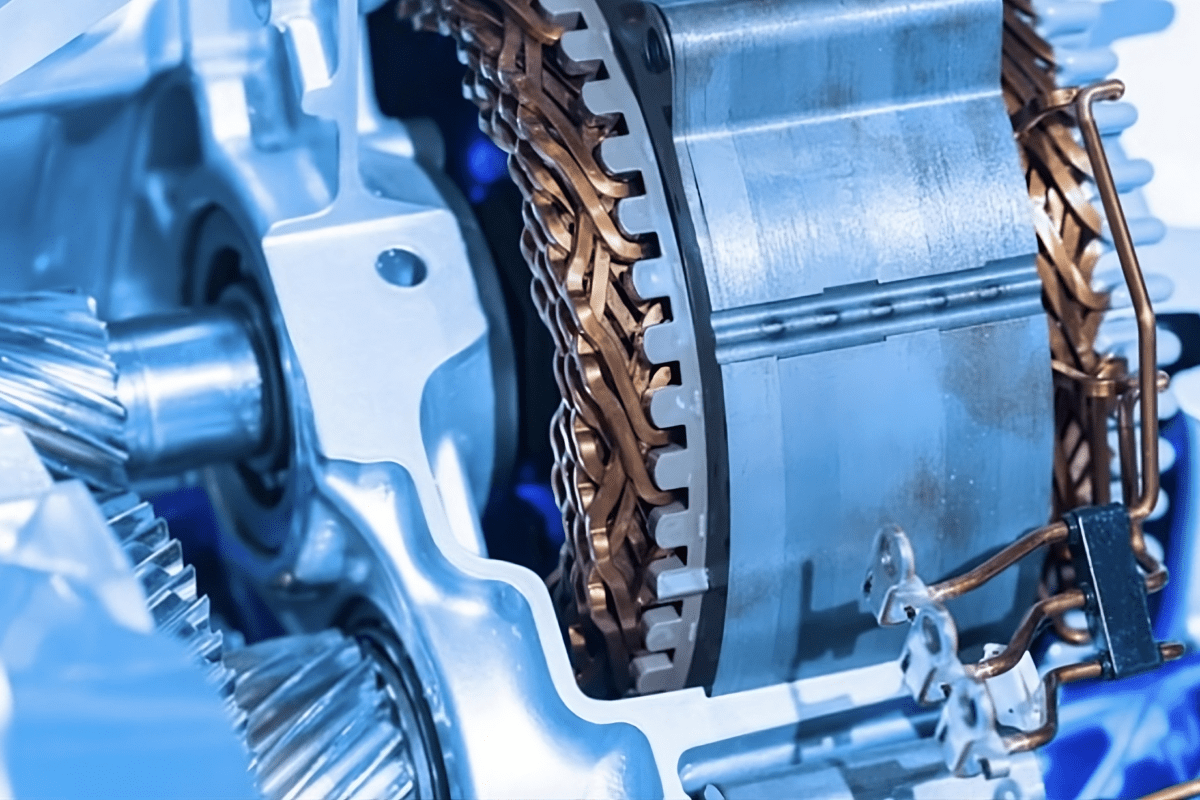

Annual engine output is not directly aligned to with vehicle output, but naturally the totals are in the same ballpark. Only a small part of the discrepancy between vehicle output and engine output is currently attributable to production of vehicles which require no combustion engine, namely battery electric vehicles (BEVs).

According to Germany’s Süddeutsche Zeitung, the EU is planning a €100bn (US$108bn) incentive and stimulus package to support the mobility sector, including €20bn for clean vehicles

With the proportion of BEVs and electrified vehicles on the rise, electrification is now an intrinsic part of analysis of engine production. BloombergNEF, Bloomberg’s clean energy and advanced transport information provider, notes that prior to the onset of the coronavirus crisis, there had been ten successive years of strong growth in electric vehicles, which includes battery electric and plug-in hybrids. In the latest edition of its annual EV report, ‘Long-Term Electric Vehicles Outlook’, BNEF notes the rapid growth in electric and plug-in hybrid vehicles in the second half of the last decade: “Passenger EV sales jumped from 450,000 in 2015 to 2.1 million in 2019.”

There were, however, pre-COVID signs of a slowdown in EV growth; according to Berylls Strategy Advisors, global EV sales grew annually by over 50% from 2012 to 2018, but slowed dramatically to just 5% year-on-year in 2019; despite an overall decline in global vehicle sales, this for Berylls signalled “a standstill in demand” for BEVs and PHEVs.

Whatever happened before COVID-19, however, is a mere bagatelle to the impact the pandemic will have on vehicle demand in and after 2020. BNEF notes that EVs are “more resilient” than combustion-engined vehicles in the face of the coronavirus; in 2020, it forecasts that global sales of passenger EVs will decline by 18% to 1.7 million units—dramatic, but less severe than the 23% decline it anticipates in cars with combustion engines; the research unit also expects the overall car market to decline at a similar rate in 2020.

COVID-19 will test the industry’s commitment to electrification. With the immediate need for liquidity, expensive EV programmes will be weighed up carefully against easily amortised combustion engines

With major markets in lockdown since March, vehicle sales have collapsed; in Europe, ACEA reports a 78% decline in vehicles sales in April, following a 52% drop in March. The European automotive industry alone employs 13.8 million people in 300,000 related companies, and the European Union has indicated it is prepared to support the industry. According to Germany’s Süddeutsche Zeitung, the EU is planning a €100bn (US$108bn) incentive and stimulus package to support the mobility sector, including €20bn for clean vehicles; the decision to define ‘clean’ as vehicles emitting up to 140g CO2/km will no doubt be the subject of many heated debates. There are reportedly no plans to introduce scrappage schemes like those seen after the 2008 financial crisis, but a further €40-€60bn is earmarked for investment into new propulsion technology.

Ultimately, COVID-19 will test the industry’s commitment to electrification. With the immediate need for liquidity, automakers are looking closely at every aspect of their operations, and expensive EV programmes will be weighed up carefully against easily amortised combustion engines for the popular and lucrative SUVs and crossovers that dealers can shift more easily. Automakers in Europe in particular must balance the need to bring EVs to market for compliance reasons, with the need to protect cash and delay less profitable activities.

Any delays, however, will only be short term; even as policy and regulations get tighter, lithium-ion battery prices are falling, making EVs an ever-more attractive prospect for potential buyers. And innovation in electrification is rising; Automobilwoche reports that in 2019, German automakers and suppliers filed 660 patents for vehicles with e-motors, 42% more than in 2017. EV choice is on the up, too, and BNEF expects 500 EV models to be on the market by 2022. The impact of COVID-19 will put a significant dent in car sales for the next several years, but there are also signs that the coronavirus has generated additional interest in EVs.

This, then, brings us back to the longer-term prospects for the world’s engine plants. BNEF notes in its report that 3% of global car sales in 2020 will be electric, and 7% in 2023; by 2040, that proportion rises to 58% of new passenger car sales worldwide. Included in this number are plug-in hybrids, so more than 42% of new passenger car sales in 2040 will still use a combustion engine. Nonetheless, the writing is on the wall for the ICE, and for a significant number of the world’s engine plants.