China has sent a strong signal to the hydrogen fuel cell vehicle (FCV) industry with some major policy moves in recent months. First, hydrogen was listed as an energy source in a national law for the first time, in the Energy Law of the People’s Republic of China (draft for consultation). Then, promotion policies for FCVs were separated from those of plug-in electric vehicles (PEVs) in the Notice on Optimizing Fiscal Subsidies for Promoting New Energy Vehicles (NEVs) from four central ministries. A subsequent document that contained details of how the new policies would be implemented was shared with select provinces for consultation.

These developments are significant. Including hydrogen as an energy source in a national law signifies its strategic importance. Hydrogen can be produced renewably and can play a major role in decarbonizing transportation. The FCV is one key application of hydrogen energy, but it’s also useful in other transport sectors such as rail, air, and sea. Although less efficient than PEVs, FCVs can more easily displace conventional vehicles when fast refueling, heavy loads, or very long trips are required. The above-mentioned Notice stipulates that current purchase subsidies for FCVs will be replaced by pilot demonstrations in select cities for an initial phase of 4 years. A big focus will be on research and application of key components, and support from the central government will be in the form of financial awards to these cities rather than purchase subsidies for consumers.

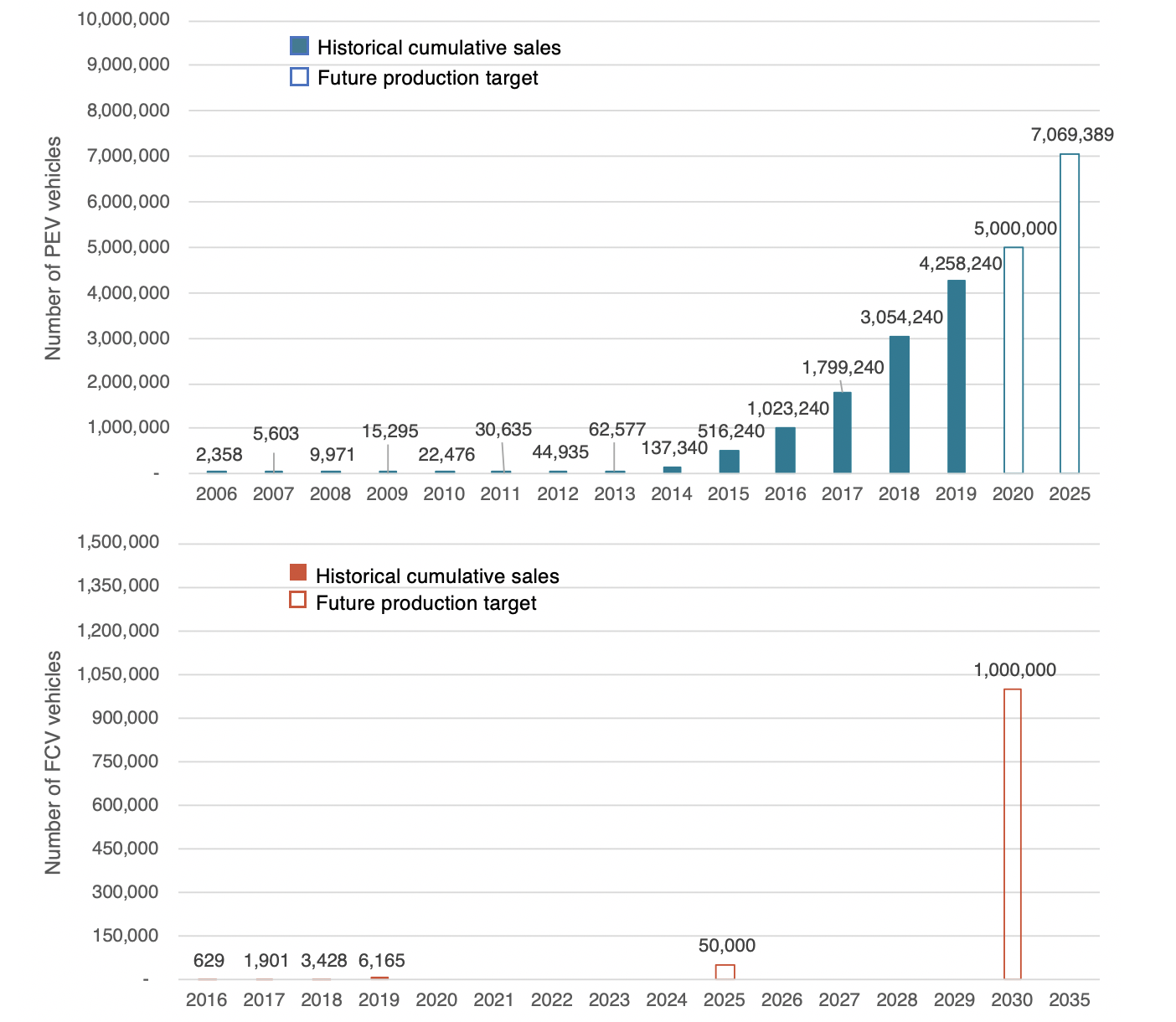

This sounds similar to the previous Ten Cities, Thousand Vehicles program, when 10 pilot cities were targeted to deploy at least 1,000 NEVs in 2009 with a one-time purchase subsidy from the central government. That program grew significantly over the ensuing years in terms of number of cities and vehicle types covered, and it drove the uptake of the PEV market. Starting with only a few hundred PEVs in 2009, China has now become the largest PEV market in the world and currently has a stock of over 3 million.

Future targets for FCVs are ambitious. From a 2019 stock of about 6,000, there is a goal to get to 50,000 in 2025, and then 1 million in 2030. Will the development of FCVs in China look like that of PEVs, or will these vehicles have their own path?

On one hand, the circumstance does look like that for PEVs in the late 2000s in several respects. First, despite years of purchase subsidies, the market is still nascent for FCVs, especially in the private sector. Sales have been increasing in the past 5 years, but there were only around 2,700 new sales in 2019. As illustrated in the figure below, this is similar to what the PEV market was like before 2009.

The small market for FCVs is due primarily to technology challenges and high costs. Currently, FCV’s main applications are transit buses and logistic vehicles because of (1) the focus on public service vehicles in the 2020 target (see the table below for details of targets); (2) lower technology requirements, due to their bigger size; (3) less challenge with charging infrastructure due to their relatively fixed routes; and (4) higher subsidies. Second, few domestic manufacturers have a firm grasp on the key technologies and many rely on imports from countries such as Japan and the United States. Third, standards and regulations are still lacking, including those regarding safety and hydrogen quality.

Another similarity is that the 2022 Winter Olympics in Beijing and Zhangjiakou could be a key opportunity for FCV development like the 2008 Summer Olympics in Beijing were for PEVs. The effort to make the 2008 Olympics “green” provided an opportunity for domestic manufacturers to develop and demonstrate their NEVs—including PEV and FCV—and this also prepared for later mass production, mostly for electric vehicles. More than 500 NEVs were in operation during the games. Similarly, according to the plan from the Zhangjiakou municipal government, there will be 16 hydrogen refueling stations and 2,000 FCVs in operation by the time of the Winter Olympic Games, set for 2022; daily hydrogen production is set to be 34.1 tonnes.

On the other hand, there are noticeable differences. First, China has learned lessons from how subsidies were granted in the early days of PEVs, as this at times led to fraud and fewer vehicles actually in operation than there were on paper. This time, in addition to a target of 1,000 FCVs at the end of the 4-year pilot for a city, average mileage of the vehicles must be over 30,000 kilometers. Also, instead of nationwide purchase subsidies, financial awards are only given to approved pilot cities which have both hydrogen energy supply capacity and enough of an economic and policy foundation to support the development of FCVs. The amount of the total available award for FCVs is set, but there is no limit for any individual city and cities that perform the best early on will receive more support than others.

Second, the focus is no longer solely on the number of vehicles deployed. The importance of the development of the whole industry supply chain for FCVs is evident from the design of the pilot program. Cities receiving financial awards have flexibility in what aspects to prioritize, including hydrogen production and transportation, key technologies and components of the fuel cell, hydrogen refueling infrastructure, and vehicle marketing. This brings many more stakeholders to the frontstage than just vehicle manufacturers, including those in energy generation, fuel cell components and materials, and special equipment. With the competition among cities and the limited total award, cities need to recognize their local conditions and make the best use of available resources. This is good on the national level, because cities can focus on their comparative advantages. The table below compares some of the key aspects of PEV and FCV planning.

| PEVs | FCVs | |

| Development target

|

2015: 500,000 annual production (~5% market share)

2020: 2 million annual production, 5 million cumulative production 2025: 25% market share |

2020: 2,000 cumulative production

2025: 50,000 cumulative production 2030: 1 million cumulative production |

| Application sector

|

Passenger cars and commercial vehicles

(bus, coach, logistics van, light truck, sanitation truck, cargo truck) |

Commercial vehicles

(bus, coach, logistics van, sanitation truck, heavy cargo truck) |

| Pilot program

|

2005: 4 cities

2010: 25 cities 2015: 88 cities 2019: nationwide |

2017: 7 cities

2019: 27 cities |

| Sales

|

2010: 7,200 (0.04% market share)

2015: 379,000 (1.5% market share) 2019: 1.2 million (6.5% market share) |

2017: 1,300 (0.004% market share)

2019: 2,700 (0.015% market share) |

| Driving policies

|

Clear goals in national industrial plans

Pilot projects Central and local subsidies Local incentives (license plate quotas, parking, traffic control) Car-sharing fleet procurement NEV mandate for passenger cars Urban bus fleet requirement Charging infrastructure planning and incentives |

Hydrogen industry development plan in pilot regions

Central and local subsidies Pilot projects Urban bus fleet requirement Hydrogen refueling station incentive |

China still has a long way to go to achieve its FCV goals. Key areas that the government can support include laying out clear pathways for hydrogen production and supply and clarifying development priorities at each stage. There is also a need to strengthen the compliance and enforcement of energy and environmental policies to accelerate clean and efficient production of hydrogen, and to encourage traditional hydrogen production industries to improve waste treatment and recycling of resources. It’s also essential to establish relevant standards and protocols such as hydrogen quality and a “cleanness” evaluation system.

Nonetheless, China has clearly learned lessons from the deployment of NEVs in the past decade and is sketching a new roadmap for FCVs. And just like PEVs, these experiences will serve as valuable lessons for others who want to develop FCVs.

SOURCE: ICCT