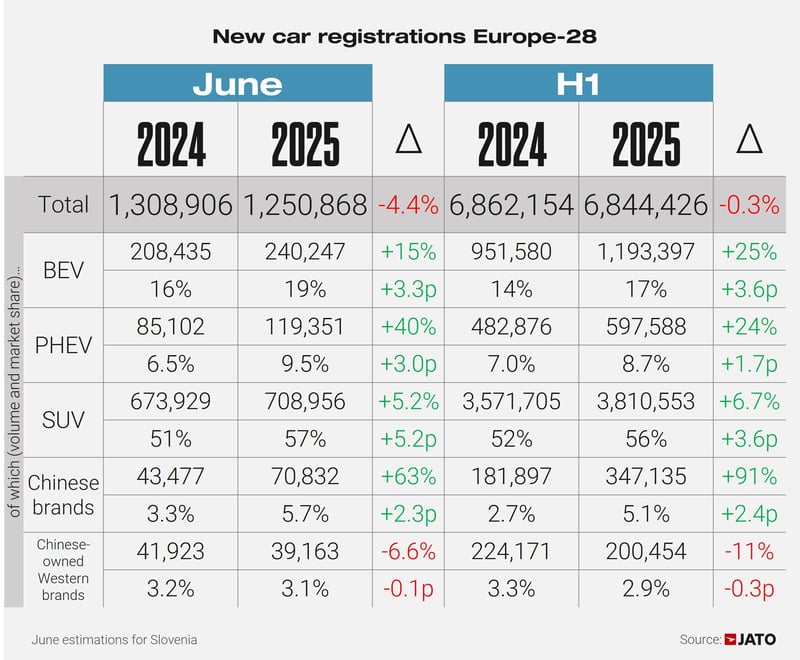

Europe’s new car market went into reverse in June, as monthly registrations dropped by 4.4% year-on-year to 1,250,868 units. JATO Dynamics’ data for 28 European markets* reveals that the decline in registrations was most in pronounced Italy (-17%), Belgium (-16%) and Germany (-14%), while France (-7%) and Switzerland (-6%) also recorded notable drops. In Romania, volumes decreased by a remarkable 50%.

June’s negative results follow months of instability in Europe’s new car market, with year-to-date registration figures totalling 6,844,426 units – a year-on-year decrease of 0.3%, or 17,728 units fewer than in H1 2024. “Persistently high prices, geopolitical and economic tensions with Europe’s trading partners, and the post-pandemic market reality are behind the decline,” said Felipe Munoz, Global Analyst at JATO Dynamics. “Western Europe has lost the equivalent of more than 2.5 million units of annual sales since 2019.”

In fact, the data shows that compared to pre-pandemic levels enjoyed in H1 2019, the market lost 1.56 million units in the first half of 2025. Proportionally, this mid-year decline exceeds the total annual losses when comparing the full year 2019 to 2024, which stood at 2.70 million units.

Chinese car brands come out on top

As Europe’s new car market has shrunk, competition has intensified – largely to the detriment of European, Japanese, Korean and American automakers. By contrast, the market share of Chinese car brands** in H1 2025 almost doubled when compared with corresponding period in 2024 to reach a new record of 5.1%. Their volume increased by 91%. Year-to-date, these brands fall just short of Mercedes at 5.2% share and ahead of Ford at 3.8%. Combined, Chinese car brands outsold Mercedes in June.

Five automakers are driving this rapid growth: BYD, Jaecoo, Omoda, Leapmotor and Xpeng. BYD, which has been particularly aggressive in its pricing strategy, registered 70,500 units in H1 2025 – a year-on-year increase of 311%. In June alone, BYD registered 15,565 units, entering the top-selling 25 brands and outselling Suzuki, Mini and Jeep. The BYD Seal U was along with the Volkswagen Tiguan the top-selling PHEV in Europe in June, and the third in H1.

Jaecoo and Omoda, both part of Chery, also made substantial progress, although this has not been due to their electric line-up. Plug-in hybrid SUVs accounted for 29% of their combined monthly registrations in June, while traditional ICE models made up almost two-thirds (63%) of the total. The Jaecoo 7 was Europe’s 9th top-selling PHEV in June.

Leapmotor registered over 8,300 units in June alone – driven largely by the popularity of its T03 city car and C10 SUV. Meanwhile, Xpeng has emerged as the most successful high-end Chinese car brand in Europe so far in 2025, with 8,338 units registered in the first half of the year. Its growth has been led by strong demand for the G6 SUV, which accounted for 5,615 of those registrations.

Major players lose market share

While Chinese car brands continued their remarkable ascent, some of the industry’s biggest players have conceded market share. Stellantis experienced the largest decrease in the first six months of the year, with its market share declining from 16.7% to 15.3% year-on-year. In fact, the group recorded its lowest H1 registrations volume across Europe-28 since its creation in 2021.

Of the ten Stellantis brands available for purchase in Europe, only three recorded growth in H1 2025: Alfa Romeo (+33%), Peugeot (+6%) and Jeep (+2%). Overall, Stellantis saw its volumes fall by 8.6% and 11.7% in H1 2025 and June, respectively, with Fiat, Lancia, DS, Maserati and Abarth recording steep losses. Citroen and Opel/Vauxhall also posted double-digit drops in registrations. “Stellantis’ woes are a result of two factors: the failure by many of its brands to introduce new models, and its growing focus on BEVs – typically more expensive than ICE models in the new car market,” Munoz highlighted.

Tesla experienced the second steepest decrease in market share in H1 2025, down from 2.4% in H1 2024 to 1.6%. Over this period, it has lost its place in the group rankings to SAIC Motor, owner of MG, which outsold Tesla for the first time. The Chinese carmaker increased its volumes by 22% to 162,153 units, compared to a decline of 33% at Tesla to 109,264 units. “The updated Tesla Model Y has so far failed to provide the expected sales boost for the brand,” Munoz noted. “At the same time, competition from BYD and Volkswagen Group is making it harder for Tesla to maintain its leadership position.”

While Tesla was Europe’s second most registered BEV maker in June, it occupied fourth position in the H1 BEV rankings, behind Volkswagen Group (28% share), Stellantis (11%) and BMW Group (10.3%).

BEVs surpass the one million units mark for the first time

The BEV segment was a bright spot in Europe’s new car market with registrations exceeding the one million units mark for the first time in the first half of the year. In total, 1,193,397 units were registered, up by 25% year-on-year. However, despite the positive trajectory, growth slowed in June with registrations rising by 15% to 240,247 units.

BEVs accounted for 17.4% of Europe’s new car market in the first half of 2025 – an increase of 3.6 percentage points compared to the same period last year. Denmark led the gains in market share increase between H1 2024 and H1 2025 (+19 percentage points) followed by Norway (+9.2), Belgium (+8.0), Finland (+7.2), and Austria (+5.6). BEVs now hold the highest market share in Norway, Denmark, the Netherlands, Sweden, and Finland, while their share remains lowest in Croatia, Slovakia, Romania, Poland, and Italy.

As a segment, BEVs continue to grow in importance for most of Europe’s biggest carmakers. JATO Dynamics’ data shows that, excluding Tesla, BYD is the OEM most dependent on the segment, which represent almost two-thirds (64%) of its total sales mix. However, similar to SAIC – which saw its BEV share drop to 15.4% – BYD’s BEV share has declined compared to H1 2024. This shift reflects a strategic pivot toward other powertrains, as both manufacturers sought to mitigate the impact of tariffs imposed on their BEVs.

In contrast, Ford saw a notable increase, with BEVs rising from 4.5% of its sales in H1 2024 to 13.7% in H1 2025. Volkswagen Group’s BEV share grew from 10.1% to 18.7% over the same period, while Hyundai-Kia saw an increase from 12.6% to 19.1%. Growth was also recorded at BMW Group and Renault Group, with more modest gains observed at Stellantis, Toyota, and Mercedes-Benz.

Model-wise, and despite the challenges, the Tesla Model Y was once again Europe’s top-selling BEV in both June and H1 2025. June was the first month this year in which Model Y registrations did not decline. Although the increase was minimal (+0.1% vs. June 2024), it confirmed the trend that began in May, when volumes fell by just 7%. This marked a significant improvement compared to the average monthly drop of 50% recorded between January and April.

Renault Group tops the model rankings

Renault Group topped the model rankings in both June and the first half of 2025. More than 27,200 units of the Renault Clio were registered in June – over 3,000 more than the Tesla Model Y, which ranked second with more than 23,800 units registered during the month. Over the first six months of the year, the Renault Clio was surpassed only by the Dacia Sandero, another model from within the Renault Group portfolio.

Among the big monthly winners during June were the Clio (+19%), Peugeot 208 (+16%), and Opel/Vauxhall Corsa (+12%). Further down the rankings, year-on-year growth was recorded by the Ford Puma (+15%), BMW X1 (+27%), Mini Cooper (+25%), Opel/Vauxhall Mokka (+21%), Mercedes GLA (+20%), BMW X3 (+22%), MG HS (+36%), and Mercedes GLC (+31%).

Strong performers from the first half of the year include the Volkswagen Tiguan (+28%), MG ZS (+26%), Peugeot 3008 (+40%), Skoda Kodiaq (+30%), Jeep Avenger (+34%), Volkswagen ID.4 (+38%), Suzuki Swift (+37%), Volkswagen ID.3 (+29%), MG3 (+258%), Fiat/Abarth 600 (+400%), Skoda Enyaq (+36%), and Audi A5 (+149%).

Among the newest models, the Renault Symbioz led with 41,730 units; the Jaecoo 7 registered 37,700 units; Kia registered more than 35,000 units of the EV3; the Renault 5 found 34,202 new clients; Skoda registered 34,105 units of the Elroq; the Cupa Terramar registered 29,135 units; Audi registered 25,758 units of the Q6; while Volkswagen Group registered 20,481 units of the Tayron.

*Austria, Belgium, Croatia, Cyprus, Czechia, Denmark, Estonia, Finland, France, Germany, Greece, Hungary, Ireland, Italy, Latvia, Lithuania, Luxembourg, Netherlands, Norway, Poland, Portugal, Romania, Slovakia, Slovenia, Spain, Sweden, Switzerland, and the United Kingdom. June figures for Slovenia are an estimate.

**includes Aiways, BAIC, Beijing, Bestune, BYD, Chery, Cirelli, DFSK, Dongfeng, DR Automobiles, Ebro, Elaris, EMC, Exeed, Firefly, Forthing, Geely, GWM, Hongqi, ICH-X, JAC, Jaecoo, Leapmotor, Livan, Lynk & Co, Maxus, MG, NIO, Omoda, Seres, Skywell, Sportequipe, SWM, Tiger, Voyah, Xpeng, Zeekr.

SOURCE: JATO Dynamics