Our new research considers how freight intensity might develop in the coming years and how that would affect the recovery of US freight and logistics. We took as our base case a macroeconomic outlook, derived from McKinsey’s nine COVID-19 scenarios. To this we added an estimate of freight intensity in every US sector, analyzing historical trends and considering the structural factors that may affect their recovery.

The research produced two insights for freight and logistics companies. First, full recovery will take about three to five years, a rough patch in which companies will be severely tested. Second, the recovery will differ by transportation mode and commodity. Some products, such as nonmetallic minerals, ceramic, clay, cement, agriculture and food products, and pharmaceuticals, will likely return to growth faster and more firmly than other products. Companies that can adapt their portfolios to shippers in these sectors can accelerate their own reversal of fortune, shaving as much as two years off the time needed to return to 2019 volumes. In this article, we will review the outlook for the macroeconomy and freight in specific sectors and offer ideas about how companies can best handle the bumpy return from this crisis.

A tough freight recovery, with pockets of growth

In our June 2020 survey of US executives, 44 percent said that a “muted world recovery” scenario seemed most likely: the coronavirus recurs, growth is slow, and GDP does not fully recover until Q1 2023. (We use this scenario as the basis for all analysis in this article. Other scenarios are possible and should not be discounted; see “Safeguarding our lives and our livelihoods: The imperative of our time,” for a full explanation.)

In that scenario, sectors’ recovery trajectories vary considerably (Exhibit 2). After the current contraction, services (a broad sector, including healthcare, information, communications, business services, and education) will recover fastest, reaching precrisis gross output by Q4 2022. On the other hand, wood, paper, and textiles are not expected to recover fully by 2024.

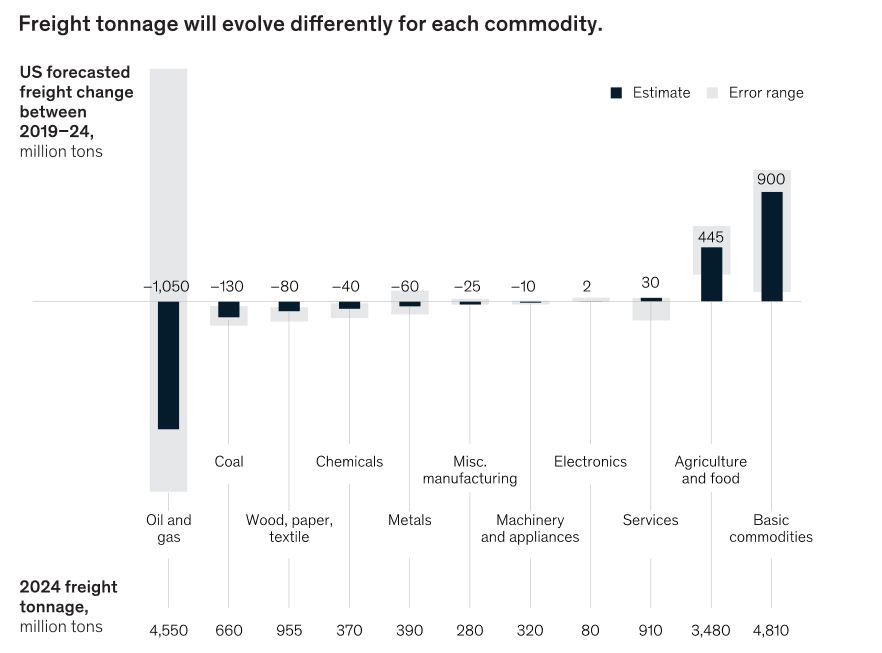

Based on our estimates of economic outlook under the “muted world recovery” scenario and changes in sectors’ freight intensity (see sidebar, “Freight intensity by sector”), we estimated the recovery in tonnage for key products (Exhibit 3). In this estimate, tonnage of basic commodities will grow significantly by 2024 due to a likely jump in freight intensity. Tonnage in goods ranging from coal to machinery and appliances will likely shrink between 2019 and 2024. Electronics, services, and agriculture and food will likely increase freight tons between 2019 and 2024 due to some combination of GDP recovery and freight-intensity changes.

Based on our estimates of economic outlook under the “muted world recovery” scenario and changes in sectors’ freight intensity (see sidebar, “Freight intensity by sector”), we estimated the recovery in tonnage for key products (Exhibit 3). In this estimate, tonnage of basic commodities will grow significantly by 2024 due to a likely jump in freight intensity. Tonnage in goods ranging from coal to machinery and appliances will likely shrink between 2019 and 2024. Electronics, services, and agriculture and food will likely increase freight tons between 2019 and 2024 due to some combination of GDP recovery and freight-intensity changes.

Effects by mode of transport

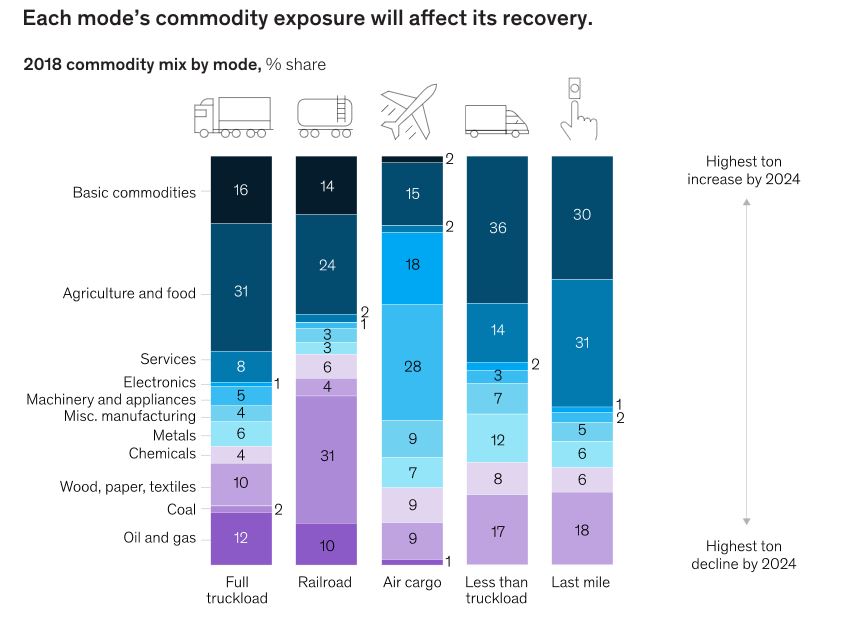

The recovery for a mode of transport as well as for individual carriers will depend on its commodity exposure, thus creating a range in performance among carriers (Exhibit 4). In most scenarios, less-than-truckload (LTL) shipping and full-truckload (FTL) shipping are likely to recover faster than other modes due to their commodity-mix profiles (Exhibit 5). Both trucking modes carry a heavy proportion of fast-to-return agriculture, food, and services and benefit from growth in e-commerce. FTL’s freight mix also contains a significant portion (16 percent) of fast-to-return basic commodities. Air cargo will take four years to recover, as light machinery (28 percent) and electronics (18 percent), two of its largest shippers, will be slower to return. Rail volumes will likely take more than four years to return, due to high exposure to slower-to-return coal, oil, and gas. Across all modes, demand hits bottom in 2020 and recovery starts afterward.

While the outlook is subdued, there will likely be pockets of growth, especially in e-commerce and last-mile delivery—opportunities that, as we discuss below, may be available even to companies whose presence in these pockets is small today. And while three to four years of recovery is no one’s idea of a picnic, the situation looks better than in 2008. After that crisis, FTL took eight years to return to precrisis levels. By that measure, the current prognosis seems mild.

How US freight and logistics companies can prepare

US freight and logistics companies are set for a moment in the spotlight—and a new kind of heft in their customer relations. Most have long felt overly managed by procurement departments. But the crisis has made logistics and transportation very much a C-suite issue, especially as shippers seek greater resiliency in their supply chains. Freight and logistics companies need to make the most of the opportunity. Transport is in for a difficult stretch, with subdued demand for the next three to five years. But the companies that can innovate and outperform their peers will have a chance to shine.

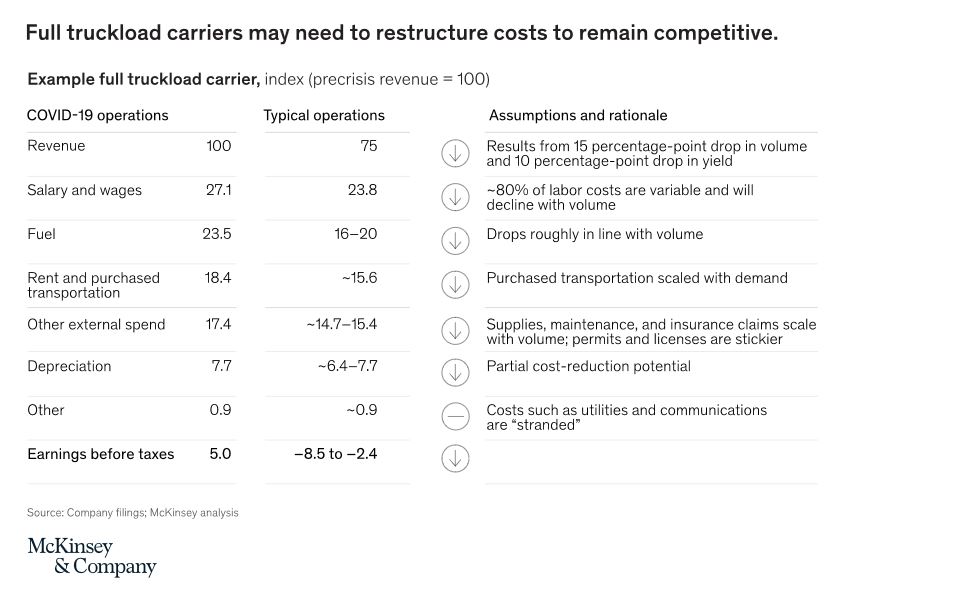

First, though, they must come to grips with the economic reality of the pandemic. Exhibit 6, an illustrative financial statement for a US trucking company, shows the potential effects. The pandemic’s demand shock is reducing volumes and yields, and could turn a company from profit to loss.

In the face of this reality, leading companies will take action across three dimensions. First, they will make bold moves on discretionary and non-people-related costs. Most logistics companies spend a significant amount on transportation, maintenance services, fuel, and parts—often up to 50 percent of their overall costs. While these costs will fall as volume decreases, leading companies are not waiting for that. Instead, they are taking this opportunity to “rebase” their spending, assess supply risks, and prepare new category strategies that will drive price and demand-side efficiencies.

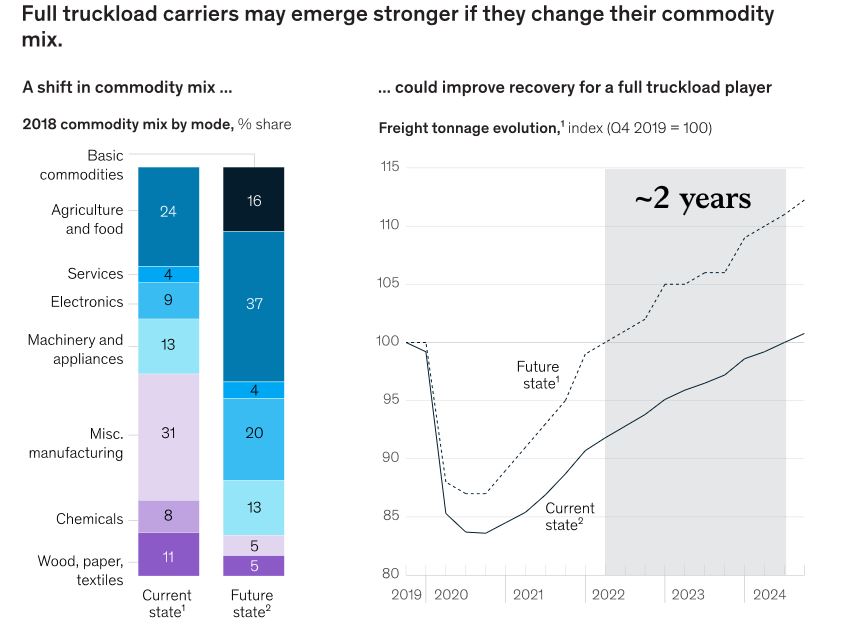

Second, companies are reorienting their commercial model toward the pockets of growth that will be stronger in the coming years. Of course, every company has key accounts and a legacy of strength in certain commodities, but companies that can find the industries and markets where growth will return faster and begin to shift resources (network, sales force, operations) to those pockets could see a faster return than competitors. For example, a representative FTL company that rebalances its mix to favor commodities that are least affected by the COVID-19 crisis can accelerate its recovery by almost two years (Exhibit 7).

Finally, leading companies are investing in new digital capabilities to unlock top- and bottom-line impact. Transportation is a business that has gone relatively undisrupted for decades—as long as freight needs to move from point A to point B, some combination of a truck, train, or plane is going to move it—and for newcomers to enter this business is not easy. While that physical movement will always remain, digital is changing the way that carriers interact with customers, raising the bar for speed and experience. This can be seen in the significant growth of some digital start-ups in recent years, as much as 50 percent faster than carriers. Leading companies realize that if they do not digitize, they may get commoditized. This kind of transformation is not easy, but success stories are appearing in the landscape and the outlook for those that wait is not looking any better. There is no better time to make the leap than right now.

SOURCE: McKinsey